2022 State of Stock Options report

10 min

0 result

This report originally appeared in TechCrunch

2022 was a painful year for startups, and startup employees. Venture capitalists tightened their investments, thousands of startup employees lost their jobs, and company valuations stalled — and in many cases fell — amid a protracted bear market.

An estimated 24 percent of startups on the Secfi platform reduced their fair market valuations in 2022.1 For people working at those startups, that means some (and in some cases, all) of their employee stock options spent 2022 underwater.

Separately, a Secfi analysis of 1,502 funding rounds from late-stage startups since March 2021 finds that startups are raising more flat rounds, and down rounds, than before.2

A number of startups that raised money in 2022 did not disclose their post-money valuations, suggesting that the true number of startups that lowered their valuations in the past 12 months could be even higher than publicly reported.

Employee stock options are a meaningful factor3 in startup compensation, and underwater stock options have the potential to negatively impact hiring and retention across the startup ecosystem. As a result, startup leaders may have to consider near-term solutions, such as higher salaries, retention bonuses, and stock option repricing.

A Secfi analysis of more than 4,300 stock option grants uploaded to the Secfi platform in 2022 shows that nearly 1 out of 4 startups reduced their fair market valuations at some point during the year.1

This year, the highest-profile example of this phenomenon was Klarna, which raised venture capital in mid-2021 at a $45.6 billion valuation, but was forced to raise a new round of funding in mid-2022 at a $6.7 billion valuation — an 85 percent decline in valuation.5

“The actual number of startups that cut their valuations in 2022 is difficult to quantify, because those that do typically don’t say so publicly,” said Natalia Sanchez, Head of Capital Markets and Strategy at Secfi. “What is clear from our platform, and from public data sources, is that a meaningful percentage of startups lowered their valuations this year, or offered their investors concessions to raise money at a flat valuation.”

Stock options are a high risk-high reward form of compensation that remains one of the most compelling drivers of startup employment and retention.

A 2018 analysis of employment data suggested that the average startup employee works for just 2 years at their company before jumping to their next opportunity.6 Underwater stock options are a problem for people who joined a startup in 2020 or 2021, and now find that their shares are worth less than when they were hired.

The average startup employee in Silicon Valley receives 12- to 14 percent of the value of their salary in the form of stock options.3 In other words, a startup worker who earns a $150,000 annual salary can expect to earn an average of $21,000 worth of stock options as part of their total compensation package.

When a startup is successful, stock options rise in value — in some cases, by many multiples of value. Stock options make up 86 percent of the total net worth of the average startup employee, according to financial data that employees voluntarily shared with Secfi.9

Underwater stock options can impact employee retention, as existing employees instead look to other startups with stronger valuation growth. As a result, startup leaders who want to retain their employees may need to consider cash and retention bonuses, higher salaries, and/or a stock option repricing program.

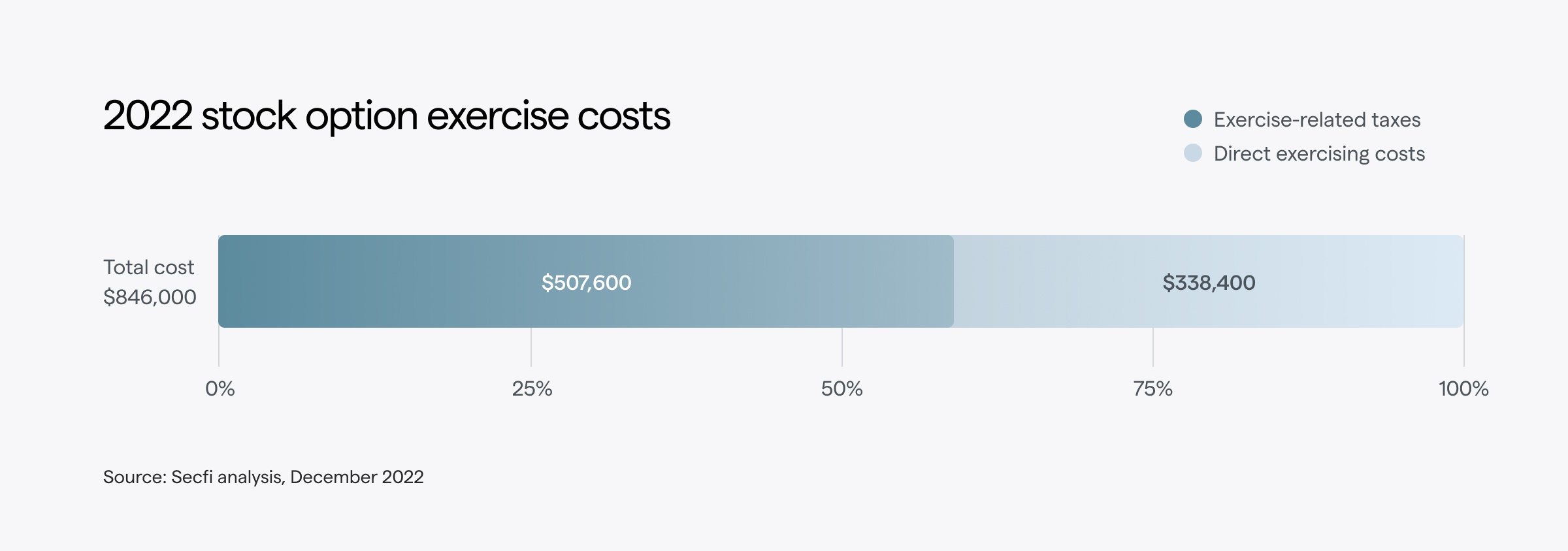

Despite economic headwinds, the cost to exercise stock options remains high.

In 2022, the average Secfi client required $846,000 to exercise their stock options and pay associated taxes. Like in previous years, taxes continue to make up the majority of the total cost to exercise.1

High costs remain a major reason why startup employees fail to exercise their stock options.

In 2022, startup employees abandoned 36- to 54 percent of their vested, in-the-money stock options, forfeiting them back to their employer’s equity pool. In doing so, the average employee walked away from $10,000 to $96,000 worth of assumed gains at the time of exercise, depending on their seniority level.3

The silver lining to a year of flat, and declining, company valuations is that a lower company valuation typically means that employees can exercise their stock options in a more tax-efficient manner.

For startup employees earning the most common type of stock options — incentive stock options — lower valuations mean that they can exercise a greater number of shares without triggering the alternative minimum tax.

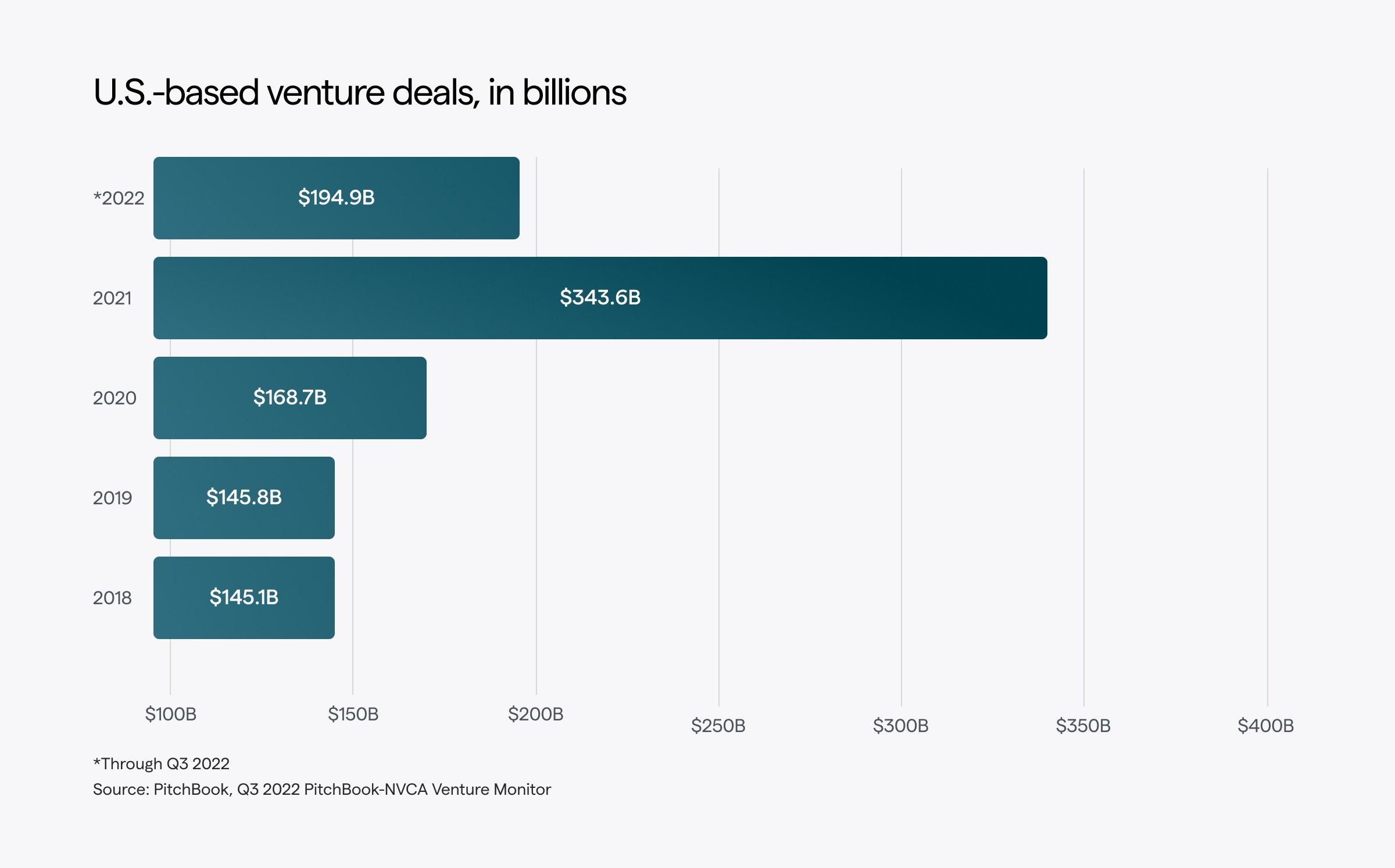

2021 represented a high water mark for startups, with U.S.-based venture capitalists investing an estimated $343.6 billion in startups, across 17,867 separate deals.4 That’s roughly $28.63 billion invested each month.

One estimate suggests that 586 new unicorns were created in 2021 alone — or roughly 11 new unicorns every week.7

Startups experienced a pullback in investments in 2022, raising $194.9 billion from U.S.-based venture capital firms in the first 3 quarters of the year — or roughly $21.65 billion per month.4

It’s estimated that there were 280 new unicorns created in the first 3 quarters of 2022 — roughly 7 new unicorns every week.8

A Secfi analysis of 1,502 venture rounds completed by late-stage companies (valued at $500 million or more) between March 2021 and September 2022 finds that valuation step-ups fell month-over-month in 2022.2

Since the market frenzy of 2021, an estimated 60 percent of late-stage companies that raised capital in 2021 raised additional capital in 2022, with the average valuation step-up in the third quarter being close to flat, at around 1.1x, according to a Secfi analysis of publicly available data.2

The data suggests one important driver of flat valuations has been the highly structured concessions that founders made with their venture investors in 2022.

In order to maintain high valuations, some startups are promising high returns to investors — conceding up to 2x in liquidation preference rights, meaning that new investors would be entitled to a return of twice their investment before common shareholders (and in some cases, previous investors) receive any money if the company exits through an acquisition.

One recent example is the fitness equipment manufacturer Tonal, which offered investors 2x liquidation preference rights during its latest fundraising efforts, according to The Wall Street Journal.

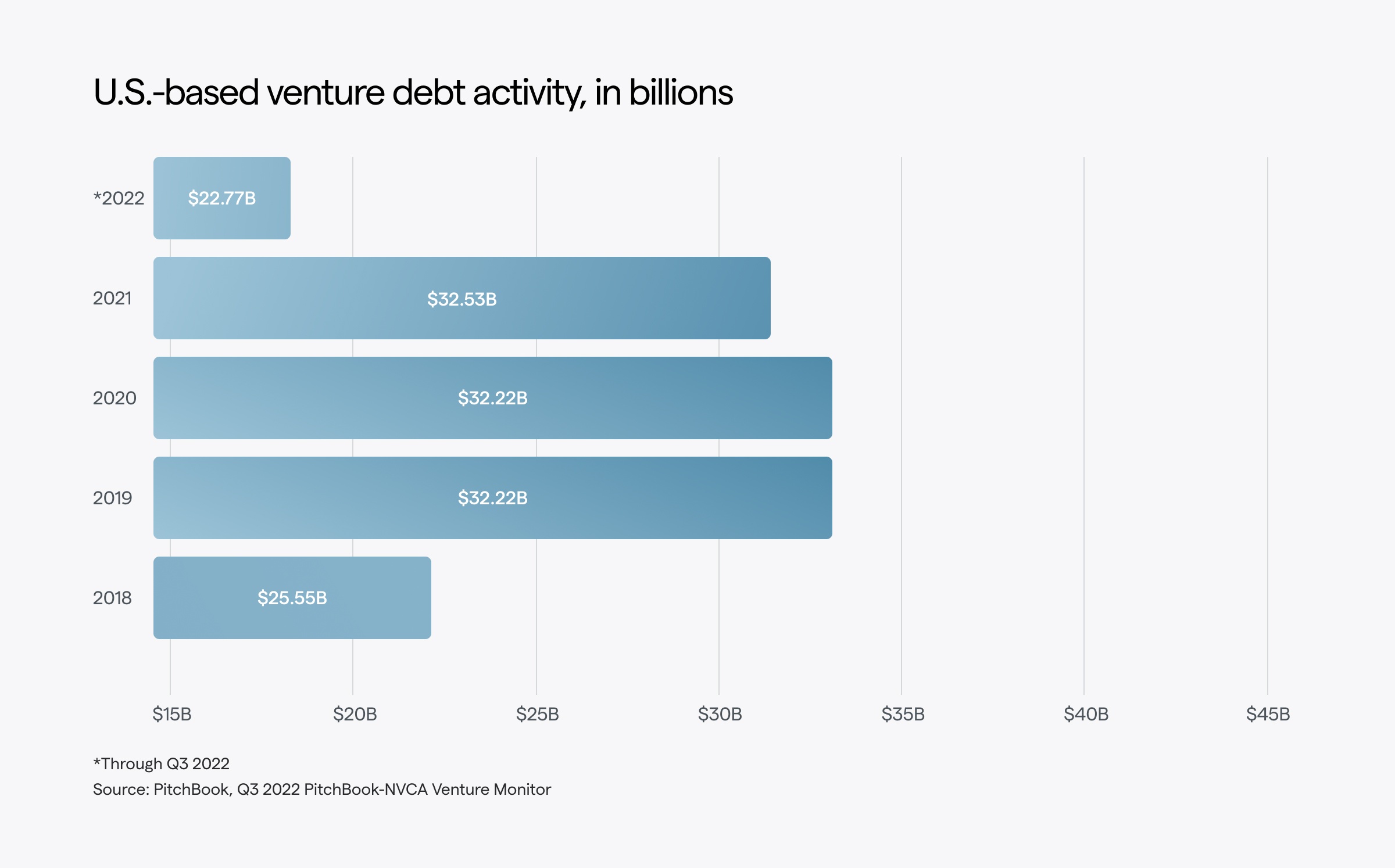

Meanwhile, U.S. venture debt activity saw fewer deals per quarter in 2022, but larger amounts of debt per deal, according to one analysis.4

In 2022, startups completed an average of 641 deals per quarter that involved venture debt, with the average deal representing $11.8 million in debt.

That compares to 2021, when venture capitalists completed 922 deals per quarter that included venture debt, with the average deal representing $8.85 million in debt.

The markets started 2022 by setting new all-time records. But rising inflation, rate hikes, the war in Ukraine, and other global economic pressures sent the major indexes into a bear market by the summer.

That pullback meant there were an average of 6 IPOs per month in 2022 — the lowest rate of IPO activity since 1990. In 2021, that rate was a little over 25 new IPOs per month.4

Meanwhile, 2022’s biggest IPOs were largely in the pharmaceutical industry, with notable listings from companies like Prime Medicine, Amylyx, and Third Harmonic Bio. Compare that to 2021 and 2022, which saw major household brands go public — Airbnb, Coinbase, Robinhood, Doordash, Snowflake, and others.

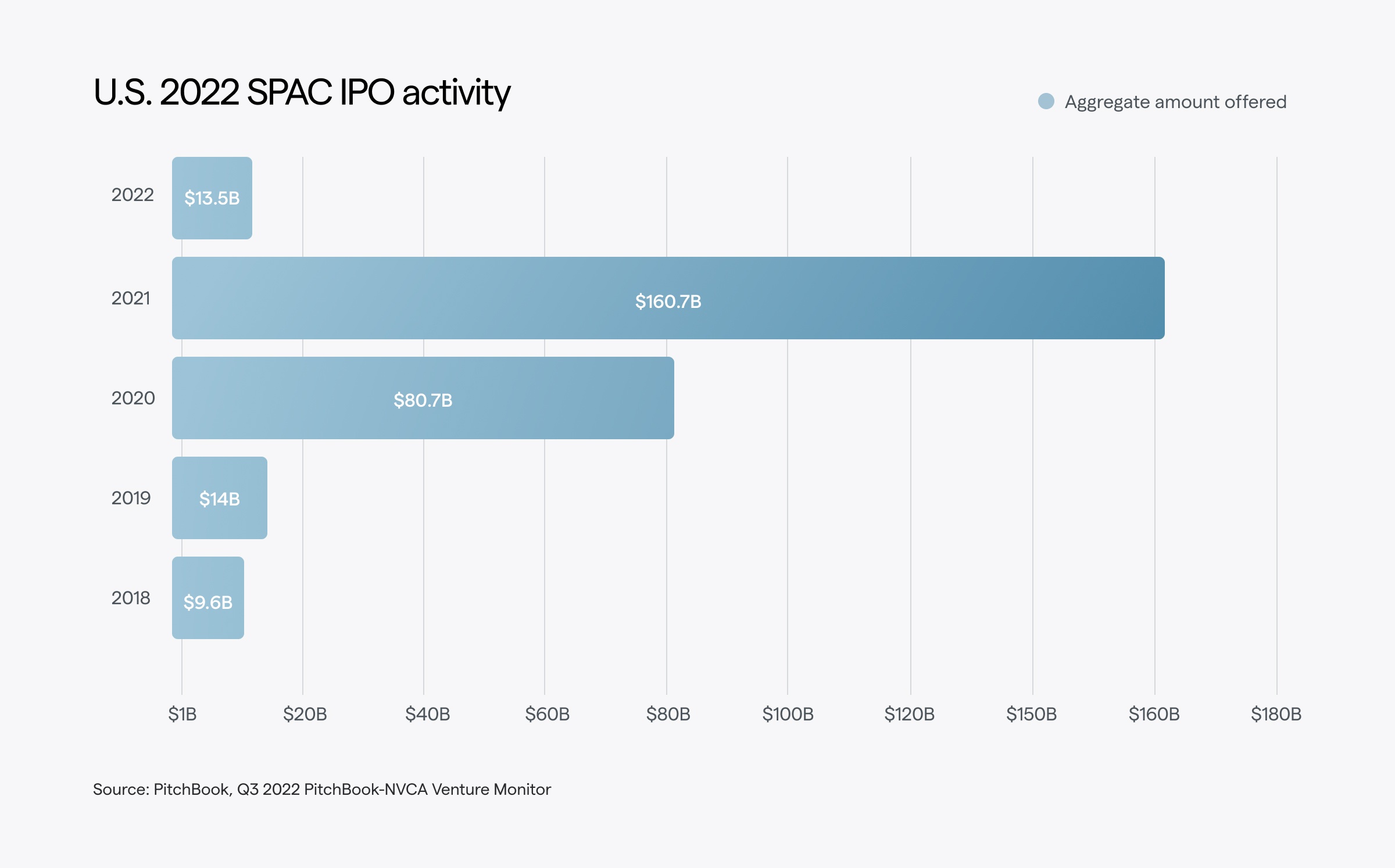

One big factor contributing to the pullback in new IPOs was the collapse of SPACs, which faced fresh headwinds in 2022. SPAC offerings have plunged deeply from their all-time high in early 2021 (when there were a little over 3 new SPAC offerings per day), to today, where there is fewer than one new SPAC offering per week.10

Nearly 800 of the 1,288 SPACs raised since 2020 have failed to find a suitable target company to merge with, and the majority of those will need to complete a merger in 2023 or face expiration.

Looking ahead, the data suggests that 2023 will continue to be challenging for late-stage startups, squeezed by unfavorable public market conditions for an IPO, dwindling cash runways, and investors who may aggressively negotiate down rounds and structured deals, to reduce their risk.

Historically, during economic downturns, the IPO closes and largely remains shut for 18 to 24 months, according to a Secfi analysis.11

For startup employees who are bullish on their company’s future prospects, opportunities will exist to earn more stock options during down rounds, and to strategically exercise their existing stock options in a tax-efficient manner.

Sources:

1) Secfi analysis of more than 4,300 stock option grants uploaded to the Secfi platform from Jan. 1, 2022 to December 2022

2) Secfi analysis of 1,502 late-stage startups that raised venture capital between January 2021 and September 2022

3) Carta, 2022 Annual Equity Report

4) PitchBook, Q3 2022 PitchBook-NVCA Venture Monitor

5) TechCrunch, July 11, 2022 article, "Klarna confirms $800M raise as valuation drops 85% to $6.7B"

6) Carta analysis, March 7, 2018, "Employment tenure at startups"

7) Crunchbase analysis, Jan. 5, 2022, "Global Venture Funding And Unicorn Creation In 2021 Shattered All Records"

8) Crunchbase analysis, Oct. 6, 2022, "Global VC Pullback Is Dramatic In Q3 2022"

9) Secfi analysis of personal financial data shared by startup employees on the Secfi platform, as of December 2022

10) S&P Global Market Intelligence, Nov. 14, 2022, "SPAC offerings, deals fall to pre-surge levels"

11) Secfi analysis of public market data, December 2022

-

© Secfi 2022 — All rights reserved. “Secfi” refers to Secfi, Inc. and its affiliates. Secfi, Inc. is a technology company offering a range of financial products and services through its wholly-owned, separately managed but affiliated subsidiaries, Secfi Securities, LLC (an SEC-registered broker-dealer and Member FINRA / SIPC) and Secfi Advisory Limited (an SEC-registered investment adviser). Access important information in our Legal Resources to learn more.

This information is provided by Secfi for educational and illustrative purposes only and is not considered an offer, solicitation of an offer, advice, or recommendation to buy, sell, or hold any security. All investing involves risk, including the risk of losing the money you invest, and past performance does not guarantee future performance. Secfi relies on information from various sources believed to be reliable, including information from its Customers, Clients, and other third parties, but cannot guarantee the accuracy or completeness of that information. Secfi, Inc. does not provide tax, legal, or investment advice.

Secfi is not affiliated with, sponsored, or endorsed by the companies listed, described, or featured on its site. Company logos or trademarks used do not imply endorsement and are the property of their respective owners.